Nation

3 workers fall unconscious after gas leak at restaurant

Badminton

Tang Jie-Ee Wei topple Malaysia Open champions in New Delhi

World

India's Bollywood star Saif Ali Khan stabbed at Mumbai home

Nation

MBPP enforces demolition of 11 illegal structures obstructing public pathways in Penang

Badminton

[UPDATE] Soon Huat-Shevon eye new milestone in New Delhi

Crime & Courts

O&G firm ordered to pay RM254k for unjust termination

NST Viral

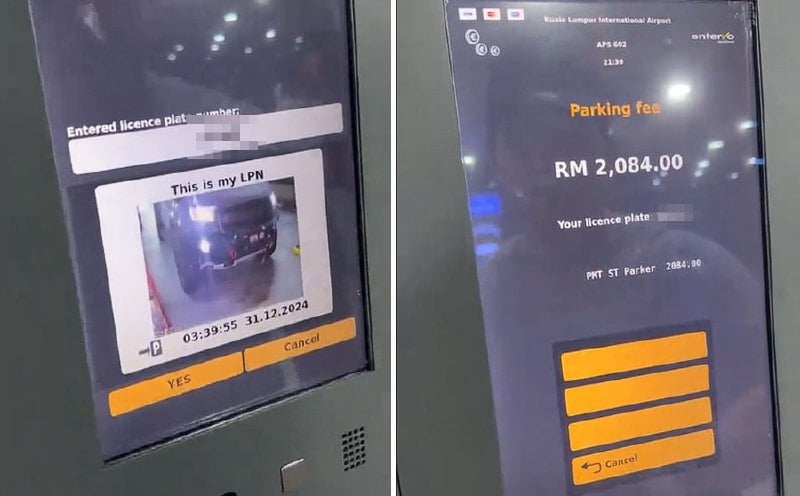

#NSTviral: RM2,084 parking fee at KLIA leaves netizens stunned [WATCH]

Crime & Courts

MACC: More bank staff to be arrested [WATCH]

Nation

3 workers fall unconscious after gas leak at restaurant

Badminton

Tang Jie-Ee Wei topple Malaysia Open champions in New Delhi

World

India's Bollywood star Saif Ali Khan stabbed at Mumbai home

Nation

MBPP enforces demolition of 11 illegal structures obstructing public pathways in Penang

Badminton

[UPDATE] Soon Huat-Shevon eye new milestone in New Delhi

Crime & Courts

O&G firm ordered to pay RM254k for unjust termination

NST Viral

#NSTviral: RM2,084 parking fee at KLIA leaves netizens stunned [WATCH]

Crime & Courts

MACC: More bank staff to be arrested [WATCH]